Trade Deficits and Solvency: Correlation not Causation

What happens if we apply Elon’s favored “first-principles” approach to trade deficits. Do we get standard economic wisdom or some contrarian miracle that justifies the Liberation Day Tariffs ?

Imagine there were only two people in the world

Imagine there were only two people in the world - Alice and Bob. Over the course of a year:

Alice buys $1,000 worth of goods from Bob (vegetables, furniture, etc.)

Bob only buys $500 worth of goods from Alice (homemade cookies, crafts, etc.)

How was Alice able to buy $1,000 of goods from Bob when she only sold $500 of goods? There are only two possibilities

Alice had saved up money - since there are only two people in this world, money just means Alice gave Bob something of value in previous years that Bob is accepting as payment now

Alice has promised to produce $500 of value for Bob in the future

Is someone getting screwed over? I’m not sure but assuming there is nothing defective in the goods Bob gave Alice, we should be more worried about Bob getting screwed over, not Alice. What if Alice is making empty promises and fails to produce the value she said she’d create?

Applying this to countries

If country X runs a trade deficit, it means it buys more in the category “goods and services” than it sells to the world in the same category “goods and services”. Therefore, it must be selling something else - something not included in the category “goods and services” to pay for this deficit.

Here are the possibilities:

(i) Country X receives more income from non-goods and services (presumably from investments abroad investments) than it has to pay out

(ii) Country X can liquidate more in foreign investments than foreigners liquidate investments in American companies.

(iii) Country X borrows from country B than Country B borrows from Country A

(iv) Country X invests in country A more than Country A invests in Country B.

Applying this to the United States

In 2024, the United States ran a trade deficit of ~$900B in 2024. The United States consumed $900B worth more goods and services produced by other countries than goods and services it sold to other countries. How did the United States pay for this?

Hypothesis 1 - Americans received more income from investments abroad than they had to pay out.

This is false. While Americans did receive investment income from foreign investments, they paid more to foreigners who invested in American assets, making the current account deficit ($1.27 trillion) even larger than the trade deficit.

Hypothesis 2 — Americans liquidated more foreign investments than foreigners liquidated American investments.

This is also false. Americans were net buyers of foreign assets, not sellers.

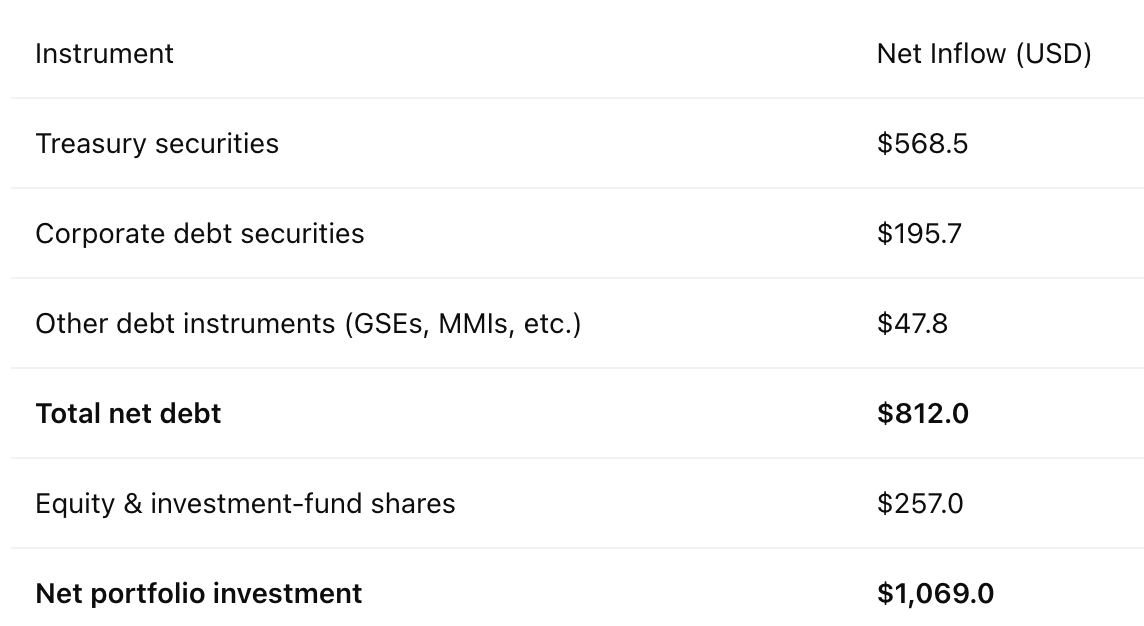

Hypothesis 3 - Americans borrowed more from foreigners than foreigners borrowed from Americans.

This is most of the answer and accounts for $934B.

Hypothesis 4: Foreigners invested more in American companies than Americans invested in foreign companies.

This is a smaller part of the answer and accounts for ~$266B

The Quality of Financing Matters

The nature of the financing matters. Currently, a significant portion of America's trade deficit is financed by an increase in government debt through Treasury securities sold to foreigners. America is borrowing from global markets to fund current consumption rather than to invest in future productive capacity.

Now imagine an alternative scenario: What if our trade deficit was primarily financed by foreign equity investments in American R&D labs and innovative companies? In that world, foreigners would be buying shares in America's productive future rather than fixed claims on dollars. They would be partners in our success rather than creditors expecting repayment regardless of outcomes.

In this scenario, there would be nothing concerning about the trade deficit. We would be importing the inputs needed to innovate and create value, with foreigners willingly participating in this process because they believe in America's capacity to generate returns. The trade deficit would represent global investment in American innovation and productive capacity, not unsustainable consumption.

The core issue, therefore, isn't the foreign share of public indebtedness but the overall level of public indebtedness and what it finances. If anything, Americans today are benefiting from this, at the expense of foreigners and future Americans.

The Reserve Currency Advantage

When foreigners buy Treasury securities, they are purchasing a claim to a fixed number of U.S. dollars in the future. But the U.S. has the unique ability to create dollars, which introduces a significant risk for these investors. If the U.S. were to significantly increase its money supply—effectively devaluing the dollar—foreign investors holding dollar-denominated debt would suffer losses in real terms.

This scenario represents a subtle form of default through inflation, where the U.S. technically repays its debts but with currency that has lost purchasing power.

What has protected the dollar from such devaluation so far is its status as the world's reserve currency. Countries hold dollars in reserve to weather economic shocks, pay for imports, service debts, and moderate the value of their own currencies. With most international obligations and transactions denominated in dollars, there's a persistent global demand that helps maintain the dollar's purchasing power.

However, this arrangement only works as long as the demand for dollars—driven by global trade and international finance—remains greater than or equal to the increase in the supply of dollars. If confidence in America's fiscal discipline erodes, or if alternative reserve currencies gain traction, the dollar's privileged position could weaken.

In a counterfactual world where most of America's public debt was held domestically rather than by foreigners, any inflation-driven devaluation would primarily hurt American citizens who hold government bonds. The inflation would effectively transfer wealth from American savers (bond holders) to American debtors (including the government itself). By having a significant portion of U.S. debt held by foreigners, some of this potential cost of inflation gets externalized—borne by foreign investors rather than domestic ones.

Solvency Over Self-Sufficiency

Think of the United States as a business: what matters is its ability to meet obligations and generate returns, not whether it manufactures every input in-house. Just as a company may outsource production if it can invest the savings into higher-return activities, the U.S. can import goods while using borrowed funds to finance projects that drive growth.

The critical measure is solvency—ensuring that the economy's growth and income streams exceed the cost of servicing its debt. A healthy business balances borrowed capital with profitable investments.

If you want to improve solvency, you have to find a way to grow revenue faster than expenses or cut expenses that don’t slash revenue as much. So if you insist on producing inputs yourself for a non-economic reason, your profitability shrinks and so does your ability to service future debt.

But Aren’t Countries Like China Cheating?

A common objection to this analysis is that other countries impose their own tariffs and trade barriers, effectively "cheating" in international trade. If countries like China are using protectionist policies, shouldn't the U.S. respond in kind?

This objection misunderstands who bears the cost of protectionist policies. When a government imposes tariffs, it's essentially holding access to its citizens hostage and making them pay more for goods while enriching cronies (domestic producers) who don't have to compete with foreign companies in their home market.

Chinese consumers pay higher prices for American goods due to Chinese tariffs. American consumers would pay higher prices for Chinese goods due to American tariffs. In both cases, the primary victims are the citizens of the country imposing the restrictions, who face reduced choice and higher prices.

If there are ways to encourage other nations to reduce their trade barriers, the U.S. should pursue them because it’s the right thing to do for the world, not because the current system is "ripping America off”.

Let's imagine if there is a fiscal surplus in the US, then where would the foreigners put those dollars? They might invest it in other countries or buy lots of shares in the US markets -- might create bubbles.

Maybe, foreigners stop devaluing their currency, making their exports more expensive. But since US demand has now dropped due fiscal discipline, I wonder if these exporters would want their exports to become expensive.

There is no scenario out of this, I guess, wherein American consumers won't have to consume a little less. Unless, countries simply pay US a tribute to be able to access their markets and using their currency and keep their own population employed.

The primary driver at the heart of it I guess is Americans now want to just consume at really low prices.

The curse of reserve currency-

The United States was experiencing the downside of its success. The dollar's status as the world's reserve currency caused its value to rise significantly, making imports cheaper. As a result, the U.S. struggled to commercialise its innovations quickly enough before China could, due in part to its complex democratic and regulatory systems that slowed the process. Consequently, the U.S. lost its competitive edge in both high- and low-tech manufacturing to China.

On the other hand, China maintained its capabilities in both high and low-tech manufacturing, allowing its commercial engines to operate efficiently. A significant misunderstanding dispelled is the belief that a thriving service industry can exist without a strong manufacturing base.

In the U.S., the standard of living was artificially sustained by a massive annual trade deficit of approximately $900 billion. Reviving the manufacturing sector will likely necessitate a significant reduction in wages and benefits.

The aim should have been a controlled lowering of debt. A $900 billion trade deficit is not sustainable for the US or the world.